Why don't Indians buy enough insurance?

A deep dive into the behavioural and cultural factors contributing to the lower adoption of insurance. 👇

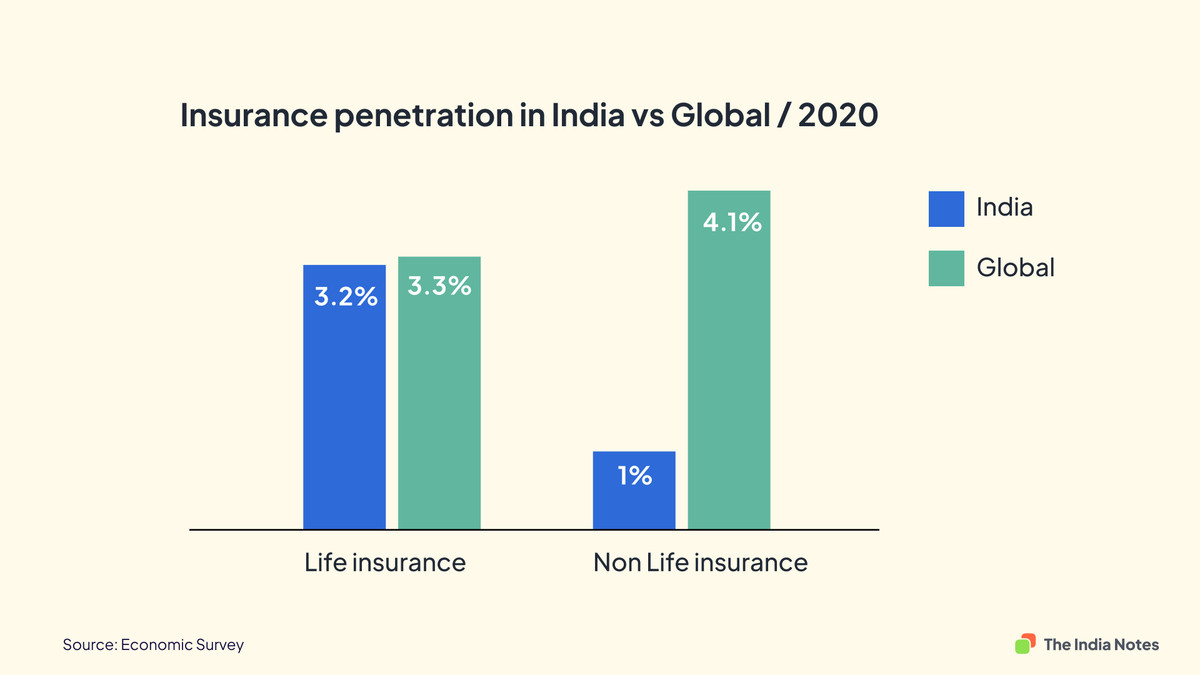

Insurance is classified as life insurance and non-life Insurance (health, motor, home, travel etc.).

Insurance penetration is measured as the percentage of total insurance premiums paid in a year to the country's GDP.

As of 2020, this is what the insurance penetration in India compared to the world looks like.

Why is there a low uptick in insurance?

Selling insurance in India is complex. Insurance provides a hedge against an individual's risk.

Hence to purchase insurance, one should come to terms with the fact that life is uncertain, and they need protection at all costs.

We build mental models to navigate life from our past experiences or the experiences of the people around us.

Hence for a healthy individual, it becomes challenging to explain the importance of health insurance.

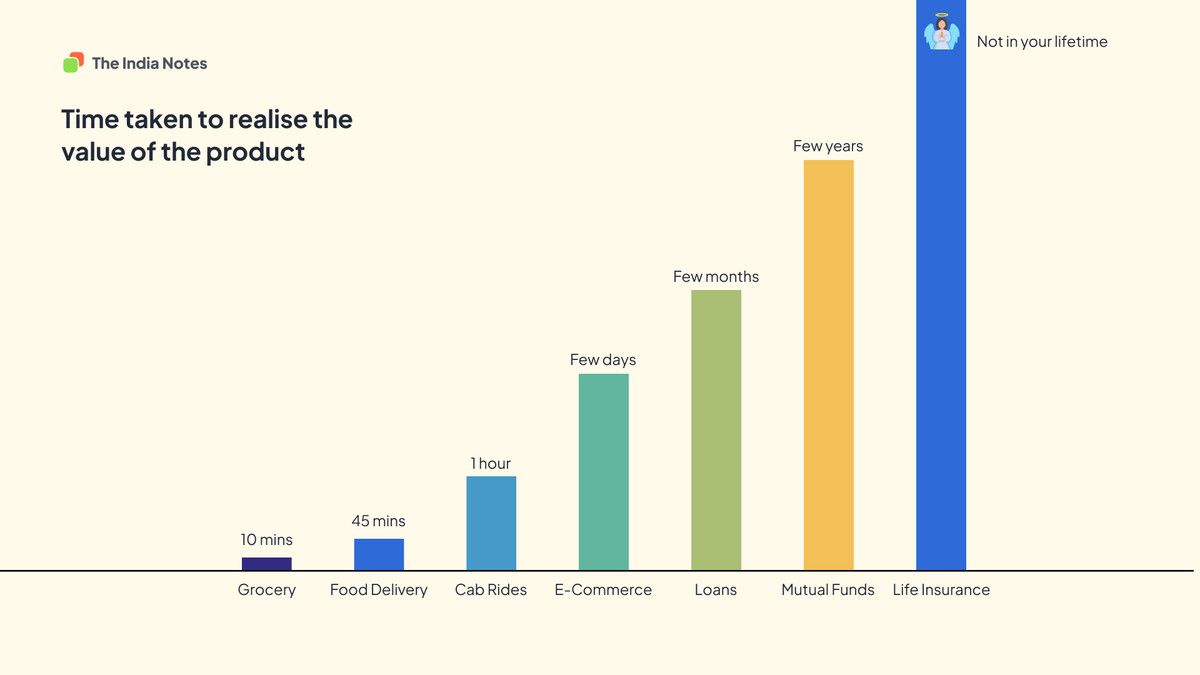

I have a funny way of thinking about this. The time taken to realise the values for most products and services ranges from a few minutes to a few years.

For example, ordering groceries takes 15 mins to reach, or mutual fund investments take a few years to realise the profit.

But a product like life insurance takes a lifetime (quite literally). One might not be alive to realise the value of the product.

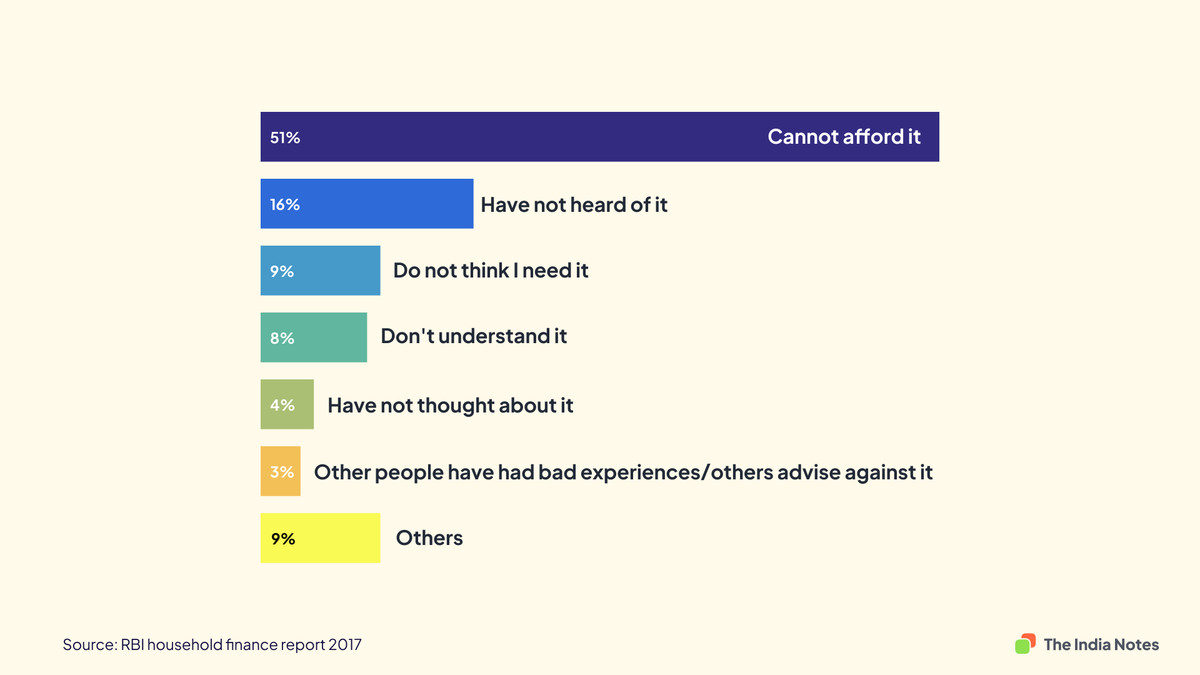

The RBI Household Finance report illustrates the reasons for low insurance purchases in India:

Let's deconstruct the top 5 reasons and the motivation behind those statements.

1. Cannot afford it:

India's per capita income is $2277 (Rs.1.82 Lakhs). Family investments and insurance become a luxury in a low-income household where most money goes into spending on basic amenities like fuel and groceries.

Even when the households start their insurance journey, the compulsion to pay monthly or periodical instalments become a burden.

India has only about 8.22 Cr income taxpayers out of 130 Cr population. Most Indians are self-employed and do not have a regular flow of income.

The irregular flow of income makes it challenging to continue a journey which expects you to pay monthly/quarterly instalments. When they skip the insurance premiums, the policy lapses, and they might have to start their journey again.

2. Have not heard of it:

Lower insurance awareness has a second-order effect on borrowing emergency loans. When individuals are not insured enough during a crisis, they resort to borrowing loans from friends, family, money lenders etc.

These sources of borrowing usually have a high-interest rate.

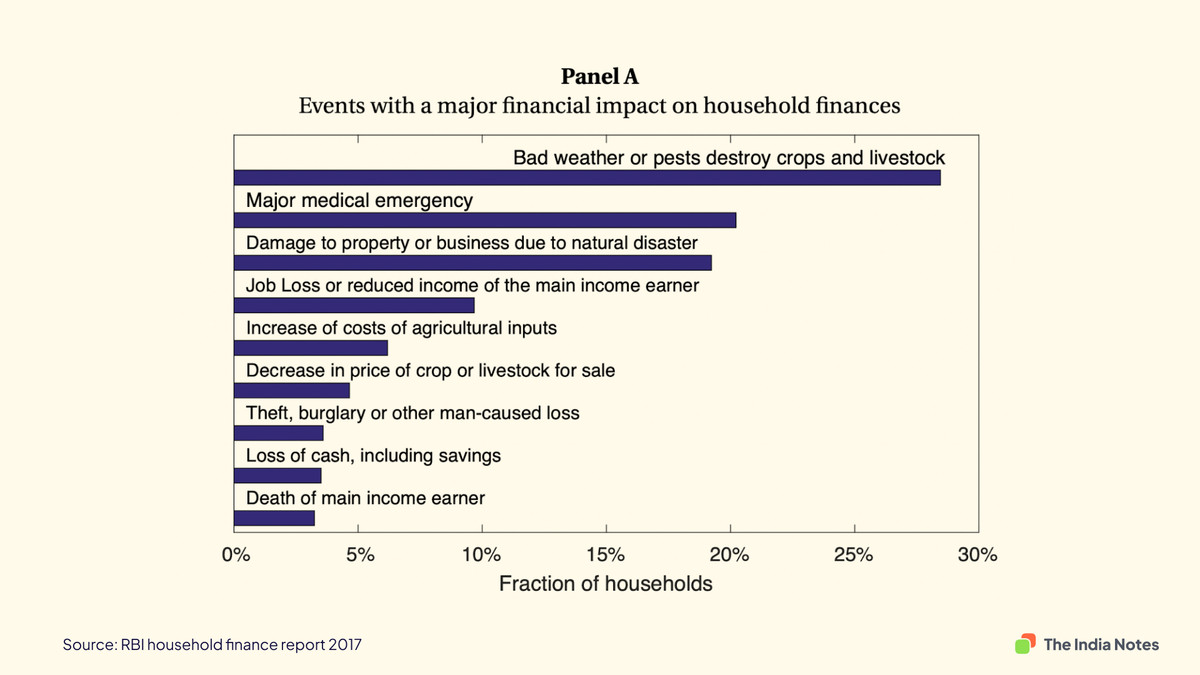

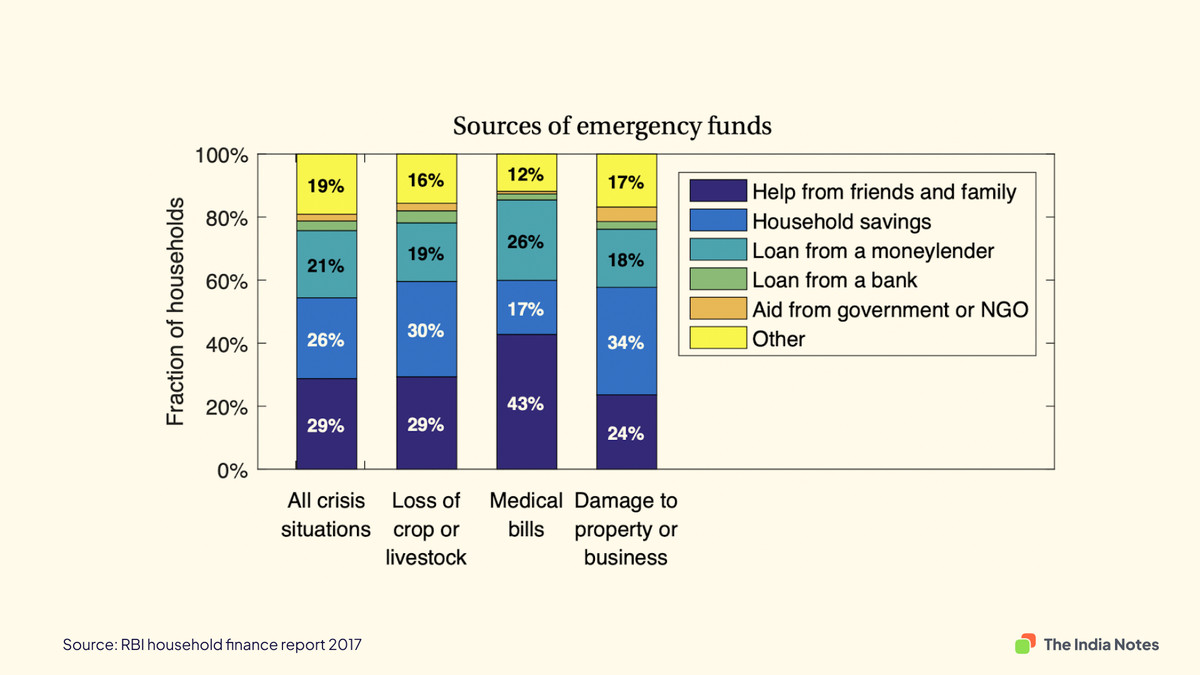

Some of the events with a major financial impact on household finances

And the sources of emergency funds

3. I don't think I need it. / Have not thought about it:

Change is hard to adapt for people. Status quo bias is where people prefer that things stay as they are or the current state of affairs remains the same.

We wish our life continues smoothly, and we believe nothing wrong will happen in the future. A common anecdotal misunderstanding is that 'If I stay healthy and keep my body fit, I wouldn't need insurance.

COVID is a black swan event. No one predicted it. But the collective suffering made us think about an uncertain future, and life is short.

The massive uptick in life insurance in India is a testament to it.

4. I don't understand it:

Buying insurance is a complex process. The overwhelming choices, paperwork, and hidden clauses make choosing the best-suited policy challenging.

With massive insurance commissions to the agents, the brokers selling the insurance products could mislead the individuals. Being transparent and reducing choice fatigue could solve this.

Better control over the information makes individuals feel control over their life.

5. Others had a bad experience:

Negativity bias is the human tendency to give more importance to negative experiences than to positive or neutral backgrounds.

Insurance companies rely on the fear of an uncertain future for the sale.

Hence, the buyers need to trust the insurer to cover the risk during a crisis. In the lack of appropriate evidence, they resort to anecdotal statements from their community to make decisions.

Moreover, negative experiences spread faster than positive ones.

These problems present an exciting opportunity for the new incumbents to make an impact.

The insure-tech sector is booming in India. In 2021, the industry saw an inflow of 800 Mn in funding. India has three insure-tech unicorns (Acko, GoDigit and PaisaBazaar)

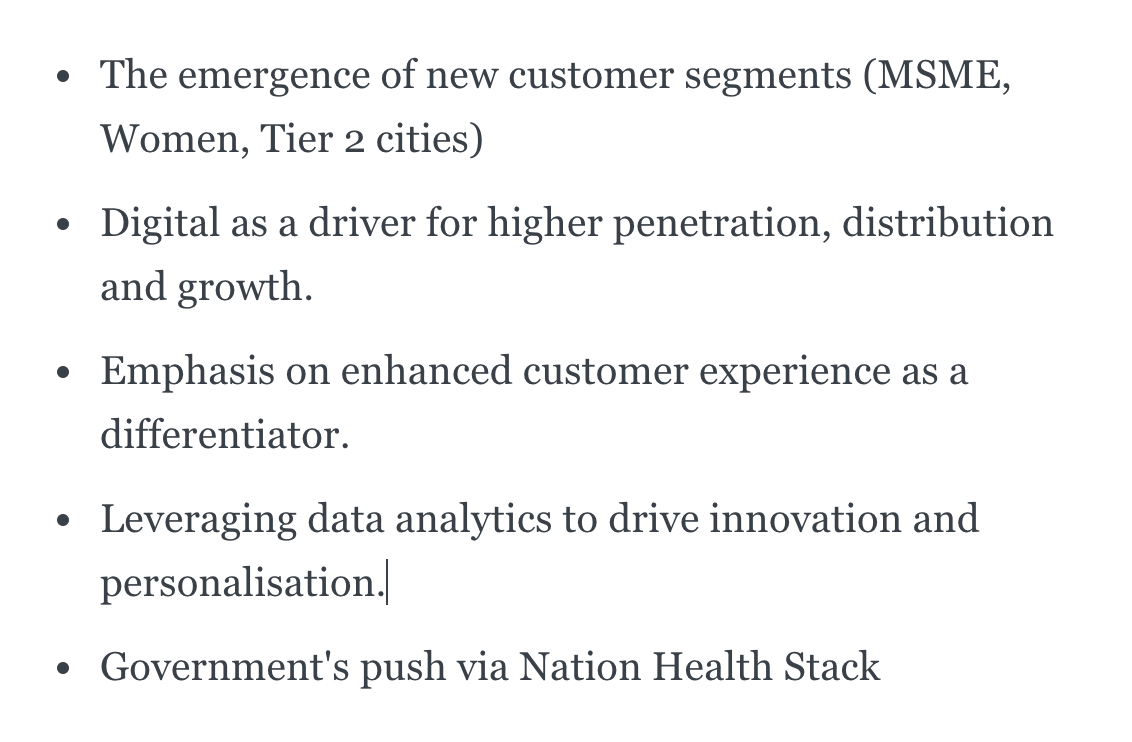

The recent insure-tech and trends report outlays five prominent themes that would improve insurance penetration in India.

You can find the full post in my newsletter 'The India Notes' where I write about Indian consumer behaviour from the lens of design and tech :)

newsletter.theindianotes.com/