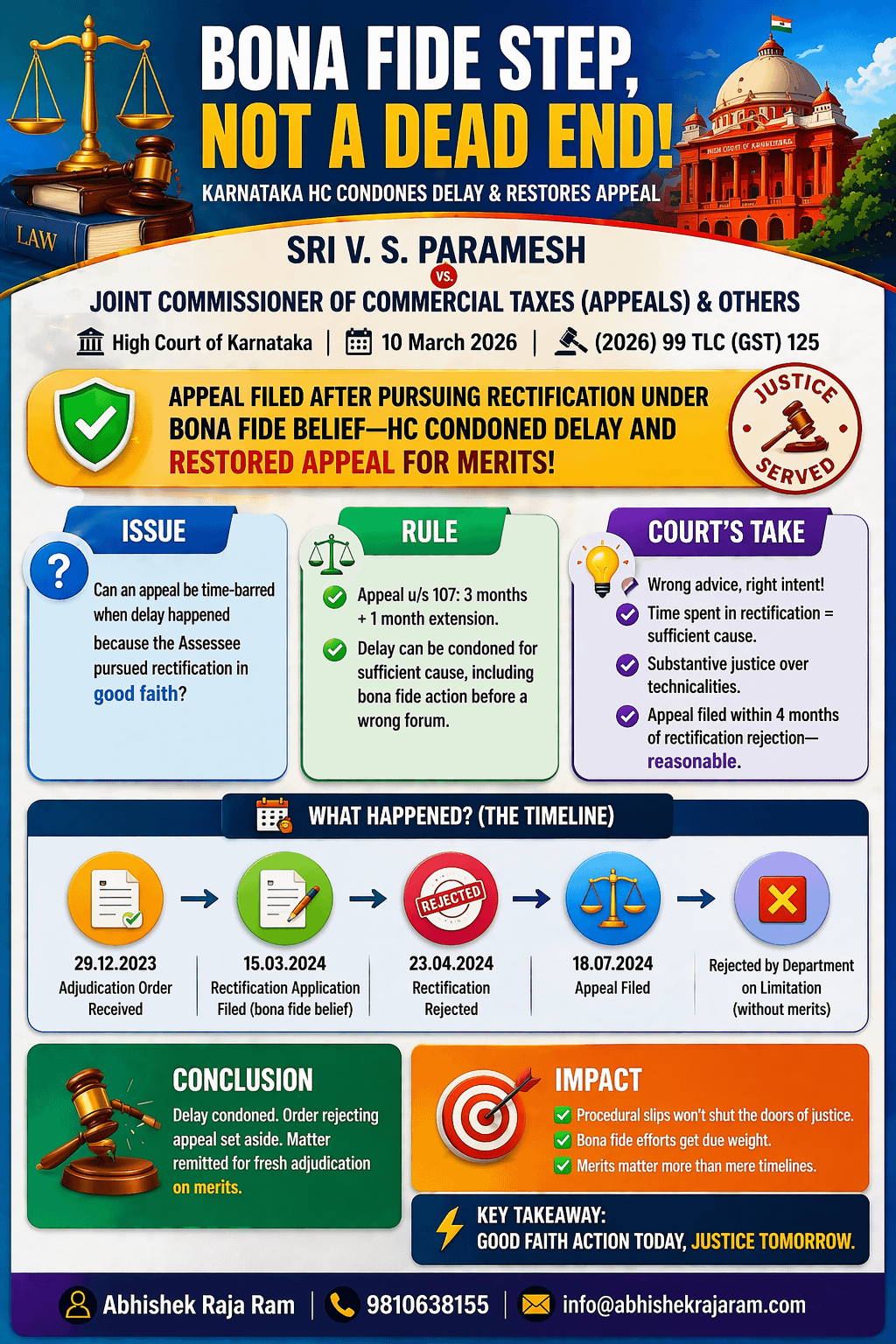

🧾 Case Title: SRI V. S. PARAMESH vs. JOINT COMMISSIONER OF COMMERCIAL TAXES (APPEALS) & OTHERS

Court: High Court of Karnataka

Citation: (2026) 99 TLC (GST) 125

Date: 10 March 2026

Headline

Assessee filed appeal after pursuing rectification under bona fide belief—Karnataka HC condoned delay and restored appeal for decision on merits.

IRAC Format

Issue

Whether the appeal filed under Section 107 of the CGST/KGST Act can be treated as time-barred when delay occurred due to time spent in pursuing a rectification application under a bona fide belief.

Rule

Under Section 107, appeal is to be filed within 3 months, extendable by 1 additional month.

However, delay can be condoned where sufficient cause exists, including bona fide prosecution before a wrong forum.

Application

• The Assessee received adjudication order dated 29.12.2023.

• Instead of filing appeal, the Assessee filed rectification application on 15.03.2024, which was rejected on 23.04.2024.

• Appeal was filed on 18.07.2024, but rejected by Department solely on limitation without examining merits.

• The Court observed that the Assessee pursued rectification under bona fide belief based on wrong advice.

• Time spent in such proceedings deserves consideration as sufficient cause.

• Appeal was filed within 4 months from rejection of rectification, thus reasonable.

Conclusion

The Court held that delay is condonable as the Assessee acted under bona fide belief.

Accordingly, the order rejecting appeal was set aside, delay condoned, and matter remitted for fresh adjudication on merits.

Impact Analysis

This judgment reinforces that procedural delays due to bona fide mistakes should not defeat substantive justice, especially where Assessee actively pursued remedies.

Abhishek Raja "Ram"

@abhishekrajaram

MEC, STBA Delhi || Speaker and Author on GST. Life dedicated towards Tax and Economic Reforms & Simplification