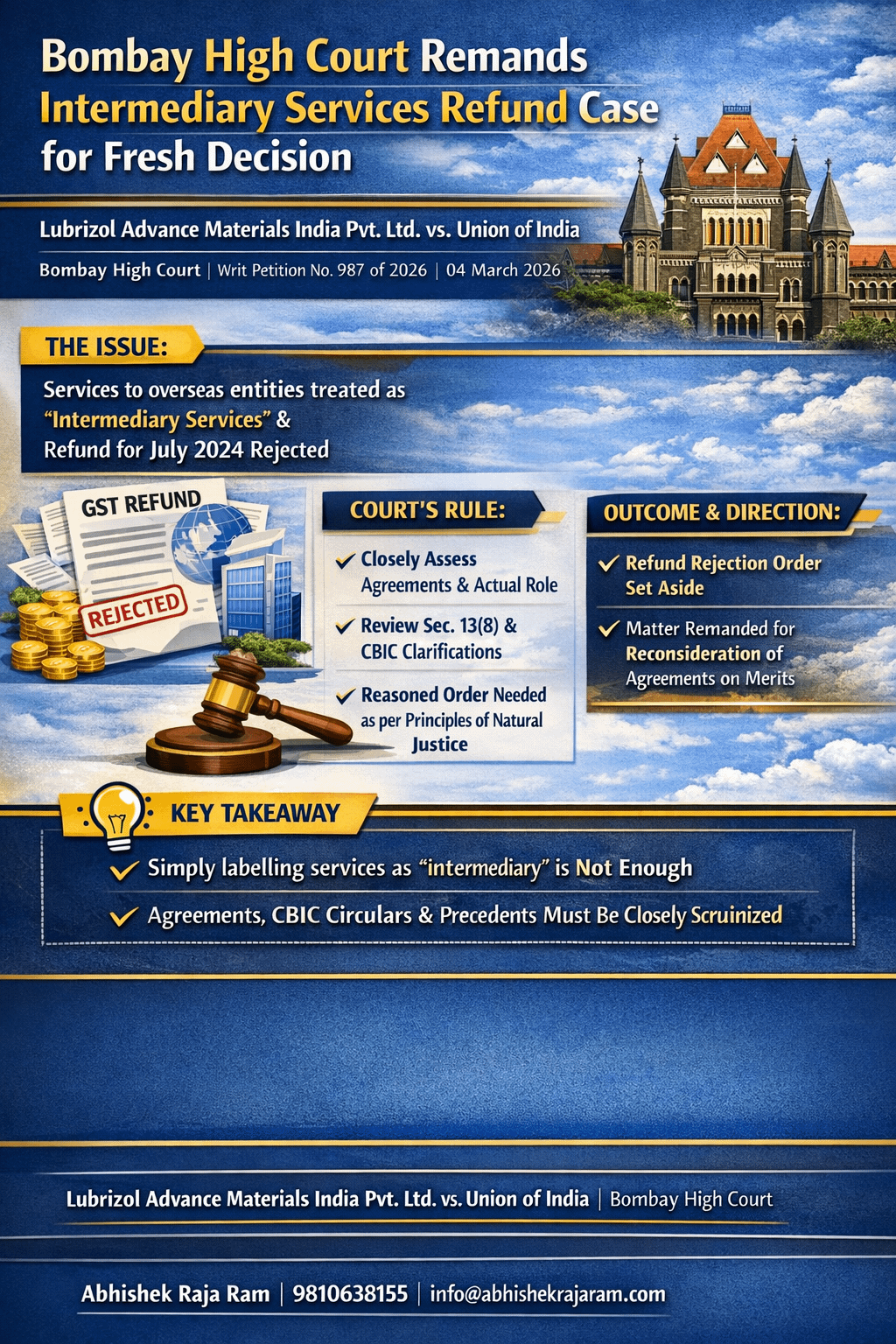

Assessee’s refund for July 2024 was rejected by treating support services to overseas group entities as “intermediary services”, but the Bombay High Court set aside the order and remanded the matter for fresh decision after proper examination of the agreements and law.

Issue

Whether the services supplied by the Assessee to its overseas group companies were in the nature of “intermediary services” under the IGST law, and therefore not “export of services”, or whether the refund rejection order was liable to be set aside for non-consideration of the Assessee’s case and lack of proper examination.

Rule

For deciding whether a supply is an “export of services” or falls within the scope of “intermediary services”, the authority is required to examine the real nature of the contractual arrangement, the role performed by the supplier, and the applicability of Sec. 13(8) of the IGST Act. An order rejecting refund under Sec. 54 cannot stand if it is passed without due consideration of the Assessee’s agreements, submissions, and the binding principles flowing from earlier judgments and CBIC clarifications. A reasoned order, consistent with principles of natural justice, is necessary.

Application

The Assessee had contended that it rendered administrative and sales support services to overseas group entities on a principal-to-principal basis, for cost-plus consideration received in convertible foreign exchange, and that in its own earlier case under the service tax regime, such services had already been held not to be intermediary services. The refund claim of Rs. 56,11,885/- for July 2024 was rejected by the Department on the ground that the Assessee was an intermediary. However, the High Court found that the impugned order required reconsideration because the authority had not properly examined the Assessee’s agreements and contentions, particularly in the light of Sec. 13(8) of the IGST Act, the CBIC circulars dated 20.09.2021, and the law laid down in Sundyne Pumps and Vistex Asia Pacific. Even the Department fairly accepted that remand would be appropriate.

Conclusion

Because the impugned refund rejection order did not reflect proper consideration of the contractual arrangement and legal position, the Bombay High Court quashed the order dated 19.11.2025 and remanded the matter to Respondent No. 2 for de novo adjudication after hearing the parties, with all contentions kept open.

Impact Analysis of this Judgment

This judgment strengthens the position that refund claims involving alleged “intermediary services” cannot be rejected mechanically without a close reading of the agreements and the actual role performed by the Assessee. It also shows that in export-of-service disputes, proper application of Sec. 13(8), CBIC circulars, and binding precedents is essential before denying refund.

Lubrizol Advance Materials India Pvt. Ltd. vs. Union of India & Ors. - Bombay High Court - Writ Petition No. 987 Of 2026 - 04-Mar-2026

Abhishek Raja "Ram"

@abhishekrajaram

MEC, STBA Delhi || Speaker and Author on GST. Life dedicated towards Tax and Economic Reforms & Simplification