Deepak Nitrite Q4FY22/FY22 results & share analysis (long term)

Company has given 5x return since Mar 2020 !! Will the good run continue? Is it a multi-bagger from current level??

A Thread 🧵👇

If you like the analysis, please retweet for support🙏

#deepakntr #deepaknitrite

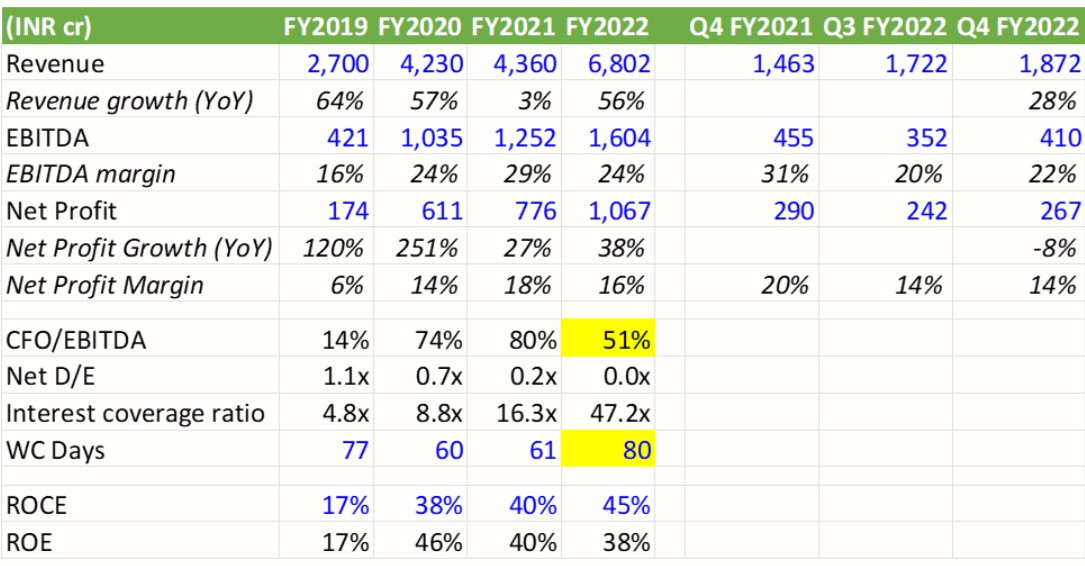

1/ Deepak Nitrite Q4FY22/FY22 results analysis [refer pic for numbers]

(a) Company has grown tremendously since FY2019 with revenue (TTM) and net profit becoming 2.5x and 6x primarily due to the Phenol business which also led to significant margin expansion.✔️

2/

(b) EBITDA margins have come down in Q3/Q4FY22 due to higher input prices. EBITDA and PAT in Q4FY22 are down on YoY basis❌

(c) Deepak Nitrite operates at a high ROE/ROCE level of around 40%✔️

3/

(d) Cash flow conversion (CFO/EBITDA) was poor in FY22 due to expansion in working capital (receivables and inventory levels) ❌

4/ Share analysis

Chemicals are all around you. And contrary to popular belief, they’re not all bad for you! Animals, plants and nearly all natural things are made of chemicals, but it’s the artificial chemicals that have the biggest impact on the world.

5/ And while artificial chemicals have earned a bad reputation, it cannot be denied that they have helped save billions of lives, increased human productivity, and completely changed the way we live. This is where Deepak Nitrite comes into play.

6/ Deepak Nitrite is a 51 years old intermediate chemicals company, with a diversified business of Basic Chemicals, Fine and Specialty Chemicals, and Performance Products.

7/ It is one of the top 3 global players in xylidines, cumidines and oximes, and a leader in India for inorganic intermediates and phenols.

8/ It retails in more than 30 countries in North America, South America, Europe and Asia. It has earned a reputation and is now a preferred supplier to multinational companies like BASF, CIBA, Monsanto and Bayer Crop Sciences.

9/ Phenolics accounted for more than 60% of the revenues and profitability in FY22. Phenolics business is cyclical in nature.

10/ Company had the advantage of high phenol prices in FY21 and some part of FY22, primarily driven by supply chain uncertainty thereby expanding the ROE/ROCE significantly, but that is unlikely to be sustainable in the medium term as can be seen in the last two quarters.

11/ With an experienced management team, and many other accolades to its name, is Deepak Nitrite really worth putting your money into?

12/ Deepak Nitrite’s product portfolio is very diverse, with historic market leadership in quite a few of them. Deepak Nitrite is trying to de-bottleneck capacity in its subsidiaries which may ensure high growth rate for the next few years.

13/ So, what is our view on the company valuation?

The Company is a high-growth import substitution story that is undertaking significant investments over the next few years to increase capacity. We can expect the revenue growth to be strong.

14/ However, investment in R&D, capex and development of new platforms is going to impact the margins of the company in the medium term.

15/ With the current PE ratio standing at 26 times and the 5-Years Price-to-earnings standing at 21 times, company seems to be overvalued at current levels.

16/ Further, Company’s majority of revenues and profitability comes from commodity business and thus it will be very difficult to sustain current levels of ROE/ROCE.

17/ As for the risks to this analysis, the volatility of prices in the industry is high and can affect margins. Moreover, any hindrance in the supply chain can affect sales.

18/ Their biggest problem, as a firm in the chemicals industry, Deepak Nitrite can be constantly under fire from environmental activism.

19/ So, would you invest in Deepak Nitrite?

Share your views in the comments and join SocInvest Community if you liked our analysis.

Join SocInvest on Telegram: t.me/+su0SABLEoedjMjI8

Share analysis article (detailed): socinvest.app/post/deepak-nitrite-currently-operating-in-a-sweet-spot

Share analysis video (English): youtu.be/AX2zm53qQVA

Share analysis video (Hindi): youtube.com/watch?v=SoB5RAcs0ZA

You can read the unrolled version of this thread here: typefully.com/_saurabhk_/EPfiu5Q

Saurabh Khandelwal

@_saurabhk_

Founder SocInvest | IIML IITKGP | All views are personal | Insignificant Investor